Many investors like bonds because they provide predictable income and lower volatility compared to stocks. But bonds come with their own challenges too.

One major problem is interest rate risk.

If you invest all your money into long-term bonds and interest rates rise later, your existing bonds may lose value. On the other hand, constantly buying only short-term bonds can limit income potential.

This is where a bond ladder strategy becomes useful.

A bond ladder is a structured investing approach designed to balance:

- Income stability

- Interest rate risk

- Liquidity

- Reinvestment flexibility

And honestly, bond ladders are popular because they offer something many investors want: a middle ground between flexibility and predictability.

What Is a Bond Ladder?

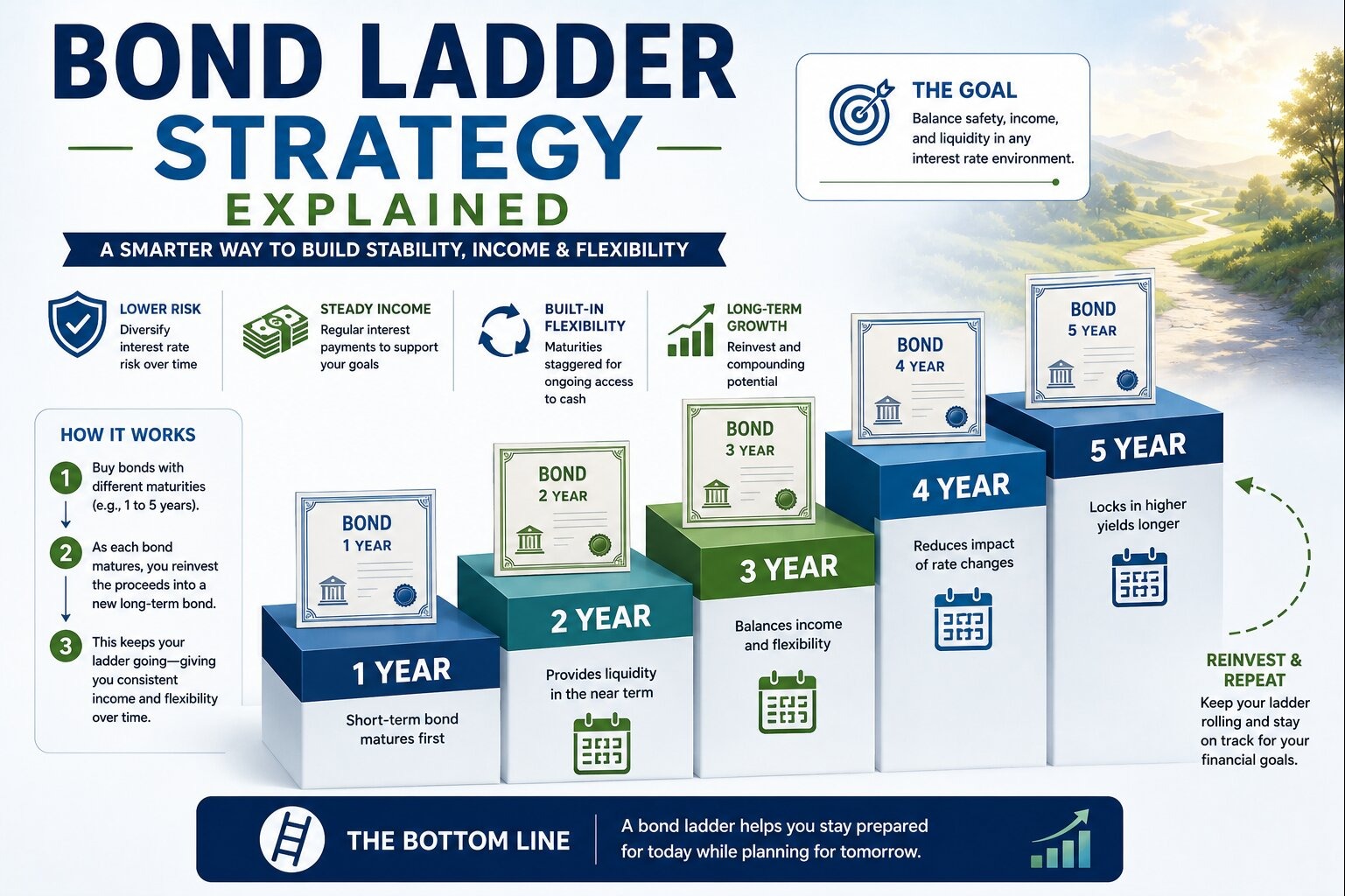

A bond ladder is a portfolio of bonds with different maturity dates spread over time.

Instead of buying one large bond with a single maturity date, investors purchase multiple bonds maturing at different intervals.

For example:

| Bond | Maturity |

|---|---|

| Bond A | 1 year |

| Bond B | 3 years |

| Bond C | 5 years |

| Bond D | 7 years |

| Bond E | 10 years |

As each bond matures:

- The investor receives principal back

- The money can then be reinvested into a new longer-term bond

This creates a continuous cycle.

Why Investors Use Bond Ladders

Bond ladders help address several common investing concerns.

Reducing Interest Rate Risk

Interest rates constantly change.

A ladder helps avoid locking all investments into one interest rate environment.

Because bonds mature gradually:

- Some funds become available regularly

- Investors can reinvest at newer interest rates over time

This reduces the risk of making one poorly timed large bond purchase.

Creating Predictable Income

Bond ladders can provide steady cash flow through:

- Interest payments

- Regular bond maturities

This appeals especially to:

- Retirees

- Conservative investors

- Income-focused portfolios

Improving Liquidity

Since bonds mature periodically, investors gain access to portions of their capital regularly instead of waiting many years for one large maturity date.

Simple Bond Ladder Example

Imagine investing $50,000.

Instead of buying one 10-year bond, you split investments evenly:

| Amount | Bond Term |

|---|---|

| $10,000 | 2-year bond |

| $10,000 | 4-year bond |

| $10,000 | 6-year bond |

| $10,000 | 8-year bond |

| $10,000 | 10-year bond |

When the 2-year bond matures:

- You receive your principal back

- You may reinvest into another 10-year bond

Over time, the ladder continues rolling forward.

How Bond Ladder Income Works

Bonds typically pay regular interest called coupon payments.

The annual interest formula looks like this:

Annual Interest = Principal * Coupon Rate

For example:

Annual Interest = 10000 * 0.05 = 500

A diversified ladder combines multiple streams of interest payments plus staggered maturities.

Benefits of a Bond Ladder Strategy

Interest Rate Flexibility

One of the biggest advantages is adaptability.

If interest rates rise:

- Maturing bonds can be reinvested at higher yields

If rates fall:

- Existing longer-term bonds continue paying previously locked-in higher rates

This balance helps smooth interest rate exposure.

Reduced Reinvestment Risk

Reinvestment risk occurs when maturing bonds must be reinvested at lower interest rates.

Bond ladders reduce this problem because only portions of the portfolio mature at any given time.

Lower Volatility

Compared to all-stock portfolios, bond ladders often provide:

- More predictable returns

- Lower price volatility

- Greater income stability

This aligns naturally with diversification concepts discussed in How to Reduce Investment Risk.

Bond Ladder vs Buying One Bond

| Feature | Single Bond | Bond Ladder |

|---|---|---|

| Interest Rate Exposure | Concentrated | Diversified |

| Liquidity | Limited | Regular maturities |

| Reinvestment Flexibility | Lower | Higher |

| Income Stability | Moderate | More balanced |

The ladder approach spreads timing risk across multiple maturity periods.

Types of Bonds Used in Ladders

Bond ladders can include:

- Treasury bonds

- Corporate bonds

- Municipal bonds

- Certificates of deposit (CDs)

Each option has different levels of:

- Risk

- Yield

- Tax treatment

You can better understand bond types in Treasury Bonds vs Corporate Bonds.

Who Benefits Most From Bond Ladders?

Bond ladders are especially popular among:

- Retirees

- Conservative investors

- Income-focused investors

- People seeking predictable cash flow

They may also appeal to investors uncomfortable with large stock market volatility.

Bond Ladder and Retirement Income

Many retirees use bond ladders to help generate stable income.

Why?

Because staggered maturities provide:

- Regular access to capital

- Predictable cash flow

- Reduced dependence on selling stocks during downturns

This can help reduce emotional stress during volatile markets.

Interest Rate Environments Matter

Bond ladders behave differently depending on interest rates.

Rising Interest Rates

Generally favorable for future reinvestment because:

- New bonds offer higher yields

Falling Interest Rates

Existing longer-term bonds may become more valuable because they pay relatively higher rates than newer bonds.

The ladder structure helps manage both environments more smoothly.

Potential Drawbacks of Bond Ladders

Bond ladders are useful, but they are not perfect.

Lower Growth Potential

Compared to stocks, bonds generally offer:

- Lower long-term returns

- Less growth potential

Complexity

Managing individual bonds requires:

- Tracking maturities

- Monitoring reinvestment timing

- Evaluating credit quality

Some investors prefer bond ETFs for simplicity.

Inflation Risk

Inflation can reduce the real purchasing power of fixed bond payments over time.

This becomes especially important during periods of rising inflation.

You can explore inflation-related investing further in Inflation-Protected Securities Explained.

Bond Ladder vs Bond Funds

| Feature | Bond Ladder | Bond Fund |

|---|---|---|

| Maturity Dates | Fixed | Ongoing |

| Predictability | Higher | Lower |

| Simplicity | Moderate | Easier |

| Diversification | Depends on size | Usually broader |

Bond funds offer convenience, while ladders provide more maturity control.

Real-World Example

Imagine two investors during rising interest rates.

Investor A

- Invested all money into one 15-year bond

- Locked into lower yields

Investor B

- Uses a bond ladder

- Has bonds maturing regularly

- Reinvests gradually at higher rates

Investor B gains more flexibility during changing rate environments.

Practical Tips for Beginners

Start Simple

You do not need dozens of bonds initially.

Even a basic ladder with a few maturity dates can help.

Focus on Quality

High-quality bonds generally reduce default risk.

Match Ladder Length to Goals

Shorter ladders provide:

- More liquidity

- Lower interest rate sensitivity

Longer ladders may provide:

- Higher yields

- Greater income potential

Reinvest Consistently

The ladder works best when maturities are reinvested systematically.

Bond Ladders and Asset Allocation

Bond ladders often fit into broader conservative or balanced portfolios.

They can complement:

- Stock investments

- Retirement planning

- Income strategies

This connects naturally with Investment Portfolio Allocation by Age.

Common Mistakes Investors Make

| Mistake | Potential Problem |

|---|---|

| Chasing risky high-yield bonds | Greater default risk |

| Ignoring inflation | Reduced real returns |

| Poor diversification | Concentrated exposure |

| Forgetting reinvestment strategy | Inconsistent ladder structure |

| Overcomplicating the ladder | Difficult management |

Final Thoughts

A bond ladder strategy offers a practical way to balance income, flexibility, and interest rate management within a fixed-income portfolio.

By spreading bond maturities across different time periods, investors may reduce:

- Interest rate risk

- Reinvestment risk

- Liquidity concerns

At the same time, bond ladders can provide more predictable income and portfolio stability.

And honestly, that balance is exactly why many conservative and retirement-focused investors appreciate bond ladders so much. They are not designed to maximize excitement or chase huge returns. They are designed to create steadier, more manageable investing outcomes over time.