Saving money is one of the most important financial habits—but understanding how your savings actually grow is just as important. That growth comes from interest.

If you’ve ever wondered how banks calculate interest, why some accounts earn more than others, or how your money increases over time, this guide will break it down in a simple and practical way.

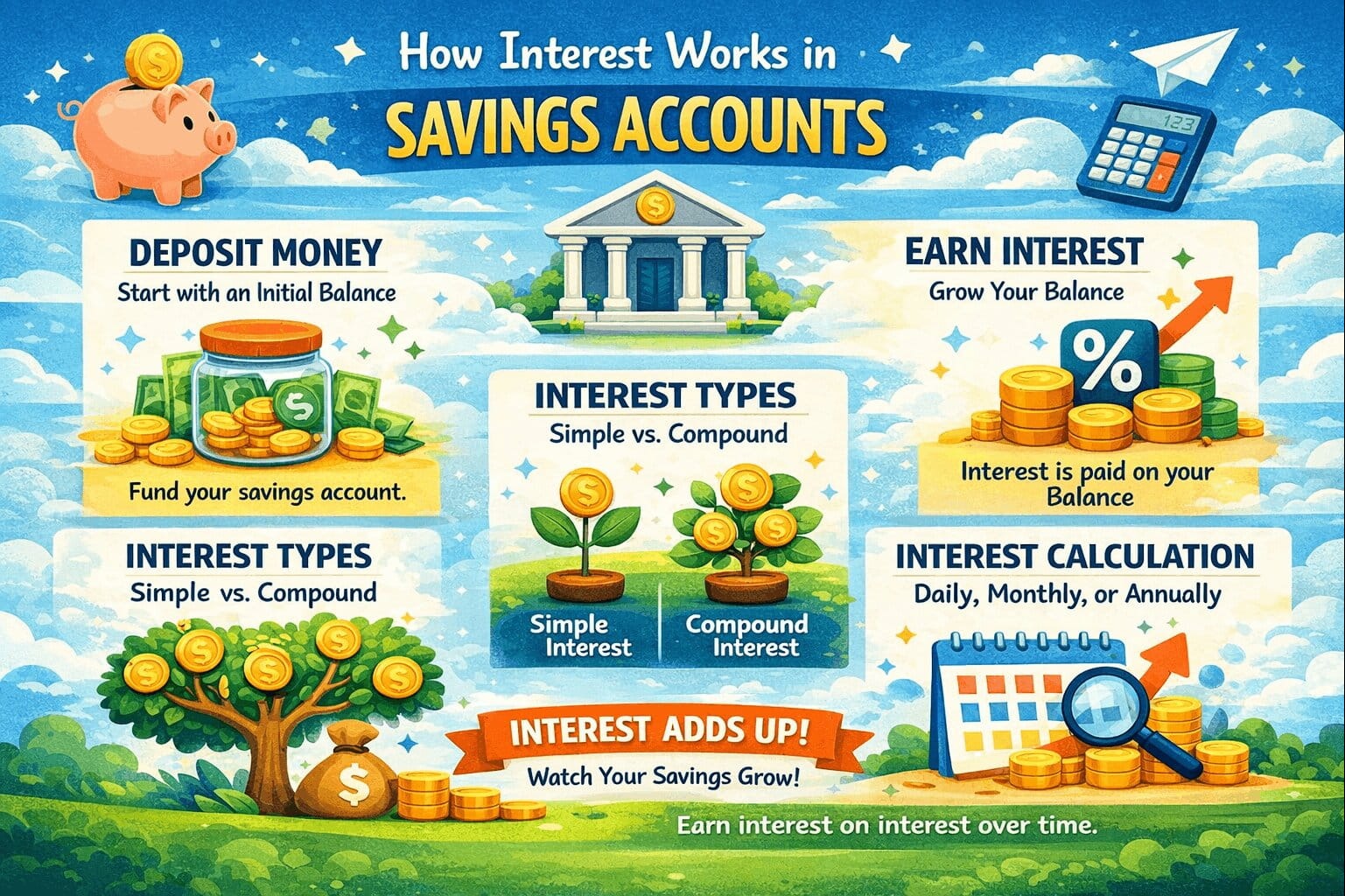

What Is Interest in a Savings Account?

Interest is the money a bank pays you for keeping your funds in a savings account.

Think of it like this:

- You deposit money into the bank

- The bank uses that money to lend or invest

- In return, the bank pays you interest

This is how your savings grow without you doing anything extra.

What Is APY?

When looking at savings accounts, you’ll often see APY (Annual Percentage Yield).

APY represents:

- The total interest you earn in one year

- Including the effect of compounding

For example:

- APY: 4%

- $1,000 deposit → $40 earned in a year (approx.)

APY gives you a clearer picture than a simple interest rate because it includes compounding.

How Interest Is Calculated

Savings account interest is usually calculated daily but paid monthly.

Here’s a simplified version of the process:

- The bank calculates your daily balance

- Applies a daily interest rate

- Adds interest to your account monthly

This means your money grows steadily over time.

The Power of Compounding

Compounding is what makes savings accounts powerful.

It means you earn interest not just on your original deposit—but also on the interest you’ve already earned.

Example:

- Initial deposit: $1,000

- Interest earned: $40

- New balance: $1,040

Next year, you earn interest on $1,040—not just $1,000.

Over time, this creates a snowball effect where your money grows faster.

Real-World Example

Let’s compare two savers.

Saver 1: No Interest

Rahul keeps $5,000 in cash or a zero-interest account.

After one year: Still $5,000

Saver 2: High-Yield Account

Amit keeps $5,000 in a 4% APY account.

After one year: Around $5,200

Over several years, the difference becomes much larger.

Simple Interest vs Compound Interest

| Type | How It Works | Growth Speed |

|---|---|---|

| Simple Interest | Earned only on original amount | Slow |

| Compound Interest | Earned on total balance (including interest) | Faster |

Most savings accounts use compound interest, which is why they are more effective over time.

Factors That Affect Your Earnings

Several factors determine how much interest you earn.

Interest Rate (APY)

Higher APY means more earnings.

Account Balance

The more money you have in your account, the more interest you earn.

Time

The longer you keep your money in the account, the more compounding works in your favor.

High-Yield vs Traditional Savings Accounts

Not all savings accounts offer the same interest rates.

Traditional banks often offer very low rates, while online banks provide much higher rates.

To understand the difference:

High-Yield Savings Accounts Explained

https://statush.com/credit-cards-banking/high-yield-savings-accounts-explained

Using Calculators to Estimate Growth

To see how your savings can grow over time, it’s helpful to use calculators.

You can try:

Compound Interest Calculator

https://statush.com/compound-interest-calculator

And for goal-based planning:

Savings Goal Calculator

https://statush.com/savings-goal-calculator

These tools help you understand how small contributions and interest rates can lead to significant growth.

How Often Interest Is Compounded

Interest can be compounded at different frequencies:

- Daily

- Monthly

- Quarterly

- Annually

The more frequently interest is compounded, the faster your money grows.

Most high-yield savings accounts compound daily, which is ideal.

Common Misconceptions

Many people misunderstand how savings interest works.

One common belief is that interest earnings are too small to matter. While it may seem small at first, compounding makes a big difference over time.

Another misconception is that all savings accounts offer similar rates. In reality, the difference between 0.5% and 4% APY can be significant.

Practical Tips to Maximize Interest

Maximizing your savings growth doesn’t require complex strategies.

Start by choosing a high-yield savings account with a competitive APY.

Deposit money regularly, even in small amounts.

Avoid frequent withdrawals so your balance can grow consistently.

Reinvest your interest instead of withdrawing it.

A Simple Way to Think About It

Interest is like your money working for you.

The more you save—and the longer you leave it—the harder your money works.

Final Thoughts

Understanding how interest works in savings accounts is a key step toward building better financial habits.

It shows you that saving isn’t just about storing money—it’s about growing it.

By choosing the right account, taking advantage of compounding, and staying consistent, you can turn small savings into meaningful financial progress over time.

It’s not about speed—it’s about consistency and letting time do the work.