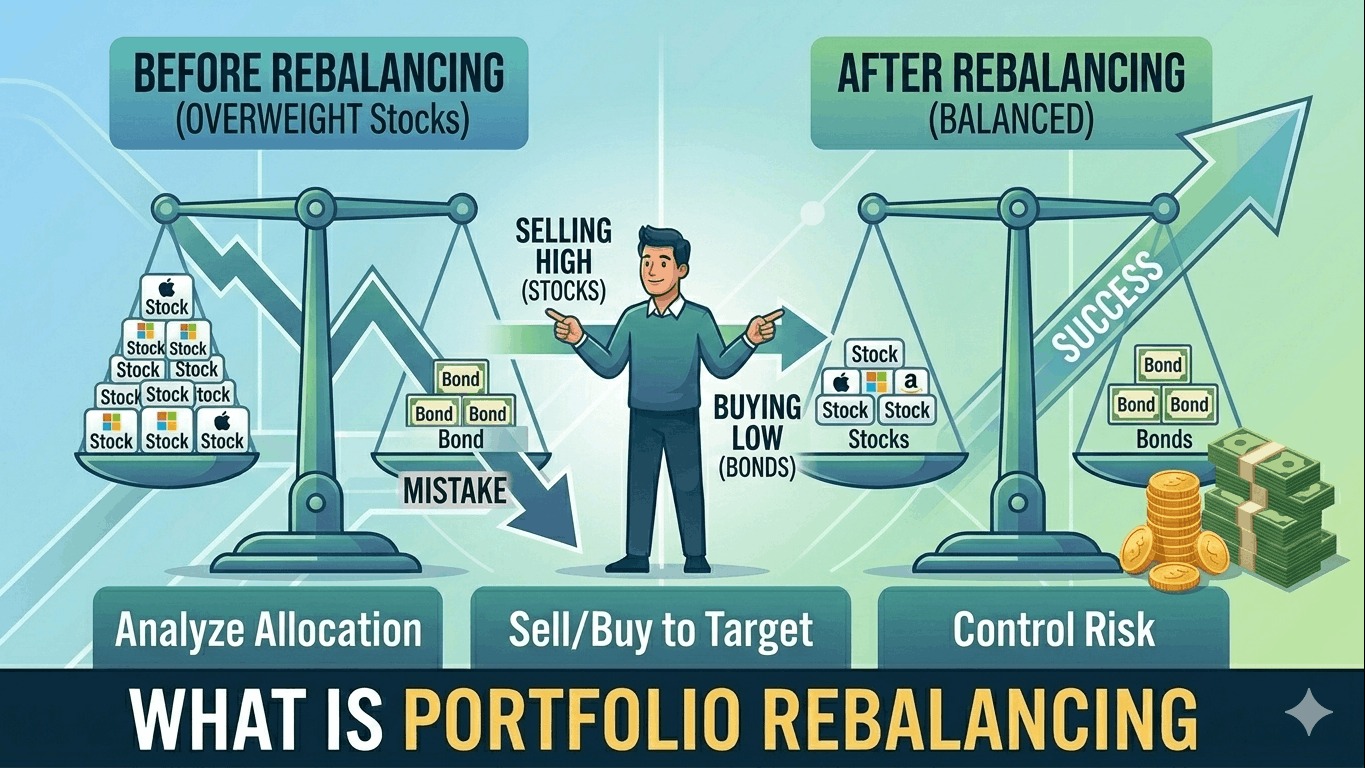

When people start investing, they often focus on choosing the right stocks, ETFs, mutual funds, or asset allocation. But one important part of long-term investing is what happens after the portfolio is built. Over time, investments do not grow at the same speed. Some rise faster, some fall behind, and your original portfolio mix can slowly drift away from your plan. That is where portfolio rebalancing comes in.

Portfolio rebalancing is the process of adjusting your investments to bring your portfolio back to your target allocation. In simple terms, it means restoring the balance you originally wanted between different asset classes such as stocks, bonds, and cash.

This concept is simple, but it plays a major role in risk management, discipline, and long-term portfolio maintenance. Many investors in the United States use rebalancing to make sure their portfolios stay aligned with their financial goals instead of being controlled by market movements.

If you are new to investing, portfolio rebalancing may sound complicated, but it is actually a practical and useful habit that can help you stay on track over time.

What Is Portfolio Rebalancing?

Portfolio rebalancing is the act of adjusting the holdings in your investment portfolio when they move away from your intended asset allocation.

For example, imagine you start with a portfolio that is:

- 60% stocks

- 35% bonds

- 5% cash

If stocks perform very well over the next year, your portfolio might shift to:

- 70% stocks

- 25% bonds

- 5% cash

At that point, your portfolio is now more aggressive than you originally planned because stocks make up a bigger share than intended. Rebalancing would mean reducing the stock allocation and increasing the bond allocation to bring the portfolio back closer to your target mix.

The purpose is not to chase returns. The purpose is to manage risk and maintain your desired investment structure.

Why Portfolio Rebalancing Matters

A portfolio can drift over time without you noticing. That drift may change your risk level in ways that no longer match your goals or comfort level.

If one part of your portfolio grows faster than the rest, it can become too large and expose you to more concentration risk. Rebalancing helps keep the portfolio aligned with your original strategy.

Here are some of the main reasons rebalancing matters.

It keeps your risk level under control

Your target allocation reflects the level of risk you intended to take. If stocks grow too large in the portfolio, your overall risk rises. Rebalancing helps restore the original balance.

It creates discipline

Investing can become emotional, especially when certain assets are doing very well or very poorly. Rebalancing adds structure and prevents decisions based only on momentum or fear.

It supports long-term planning

A portfolio should reflect your goals, time horizon, and risk tolerance. Rebalancing helps make sure market performance does not slowly turn your portfolio into something different from what you planned.

It can reduce overexposure

Without rebalancing, a strong-performing asset class may dominate your portfolio. That can leave you too dependent on one segment of the market.

How Portfolio Rebalancing Works

The basic idea of rebalancing is simple. You compare your current allocation with your target allocation. If the percentages have moved too far, you adjust the portfolio.

That adjustment can involve:

- Selling some of the assets that have grown above target

- Buying more of the assets that are below target

- Redirecting new contributions into underweighted areas

- Reinvesting dividends into the parts of the portfolio that need support

For example, if your goal is 60% stocks and 40% bonds, but market movements shift it to 68% stocks and 32% bonds, you may rebalance by moving some money from stocks into bonds.

Simple Example of Portfolio Rebalancing

Let’s say you build a portfolio worth $10,000 with this target allocation:

| Asset Class | Target Allocation | Starting Value |

|---|---|---|

| U.S. Stocks | 50% | $5,000 |

| International Stocks | 20% | $2,000 |

| Bonds | 25% | $2,500 |

| Cash | 5% | $500 |

After one year, suppose the stock market performs strongly and your portfolio grows to $11,500 with this new allocation:

| Asset Class | New Value | New Allocation |

|---|---|---|

| U.S. Stocks | $6,400 | 55.7% |

| International Stocks | $2,300 | 20.0% |

| Bonds | $2,300 | 20.0% |

| Cash | $500 | 4.3% |

Now your portfolio is overweight in U.S. stocks and underweight in bonds and cash. Rebalancing would involve adjusting the holdings to get closer to your original targets.

A rebalanced version of the same $11,500 portfolio might look like this:

| Asset Class | Target Allocation | Rebalanced Value |

|---|---|---|

| U.S. Stocks | 50% | $5,750 |

| International Stocks | 20% | $2,300 |

| Bonds | 25% | $2,875 |

| Cash | 5% | $575 |

This restores the original structure.

Benefits of Portfolio Rebalancing

Rebalancing offers several practical benefits that go beyond simply restoring percentages.

Keeps investments aligned with goals

A well-designed portfolio is built around your personal objectives. Rebalancing helps preserve that design.

Prevents one asset class from dominating

Strong market performance in one area can lead to concentration. Rebalancing helps prevent that from going too far.

Encourages buying lower and trimming higher

Rebalancing often means selling part of what has recently gone up and adding to what has lagged. This creates a disciplined, rules-based approach.

Helps control emotional investing

Without a plan, investors may keep chasing what has recently performed best. Rebalancing creates a more stable decision process.

Potential Downsides of Rebalancing

Although rebalancing is useful, it is not completely without drawbacks.

It may reduce exposure to strong momentum

When you rebalance, you may sell part of an asset class that is performing very well. In some cases, that asset may continue rising after you trim it.

It can create taxes or transaction costs

In taxable accounts, selling investments may trigger taxes. While many brokerages now offer commission-free trading, taxes can still matter.

Overdoing it can be unhelpful

Rebalancing too often may create unnecessary trades and complexity. For many long-term investors, less frequent rebalancing is enough.

Example of Rebalancing by Investor Type

Different types of investors may use rebalancing in different ways.

| Investor Type | Possible Target Allocation | Rebalancing Style |

|---|---|---|

| Young aggressive investor | 80% stocks / 20% bonds | Annual or threshold-based |

| Moderate long-term investor | 60% stocks / 40% bonds | Semiannual review |

| Conservative investor | 40% stocks / 50% bonds / 10% cash | More frequent monitoring |

| Retiree | Balanced income-focused mix | Review with withdrawal plan |

These examples are general, but they show that rebalancing depends on the investor’s overall strategy.

How Often Should You Rebalance?

There is no universal rule for how often to rebalance. The right frequency depends on:

- Portfolio size

- Number of holdings

- Risk tolerance

- Account type

- Tax concerns

- Market volatility

For many long-term investors, checking once or twice a year is enough. Others may prefer threshold-based rules that trigger action only when allocations move beyond a certain range.

The key is to avoid both extremes:

- Rebalancing too often for no reason

- Ignoring the portfolio for so long that risk drifts too far

Portfolio Rebalancing vs Changing Your Strategy

It is important to understand that rebalancing is not the same as changing your investment strategy.

Rebalancing means returning to your original plan.

Changing your strategy means deciding that your plan itself should be different.

For example:

- If you move from 70% stocks to 60% stocks because the market pushed you off target, that is rebalancing.

- If you move from 70% stocks to 60% stocks because you are nearing retirement and want lower risk, that is a strategy change.

Both can be valid, but they are not the same thing.

Is Portfolio Rebalancing Necessary for Everyone?

Most long-term investors benefit from some form of rebalancing, especially if they hold multiple asset classes. Without it, portfolios can become more aggressive or more concentrated than intended.

That said, the method does not need to be complicated. Some investors rebalance manually once a year. Others use target-date funds or managed portfolios that handle it automatically.

The important thing is not perfection. It is having a process that keeps your portfolio aligned with your goals.

Final Thoughts

Portfolio rebalancing is the process of bringing your investment mix back to its target allocation after market movements cause it to drift. It is a simple but important part of long-term investing because it helps control risk, maintain discipline, and keep your portfolio aligned with your financial plan.

For U.S. investors, rebalancing is often one of the easiest ways to manage a portfolio without constantly trying to predict the market. It reminds you that investing is not just about choosing assets. It is also about maintaining the right balance over time.

A portfolio that starts out well-designed can slowly change if left alone for too long. Rebalancing helps make sure it still reflects the strategy you intended. Whether you do it annually, by threshold, or through new contributions, the goal is the same: keep your investments working in a way that matches your long-term plan.