Paying yourself in 2026 is no longer just about moving money between bank accounts; it's about navigating the permanent tax changes of the One Big Beautiful Bill Act (OBBBA). Whether you are a solo freelancer or the CEO of a growing S-Corp, the way you "take your cut" determines your tax liability and your compliance standing with the IRS.

Here is the 2026 roadmap for entrepreneur compensation.

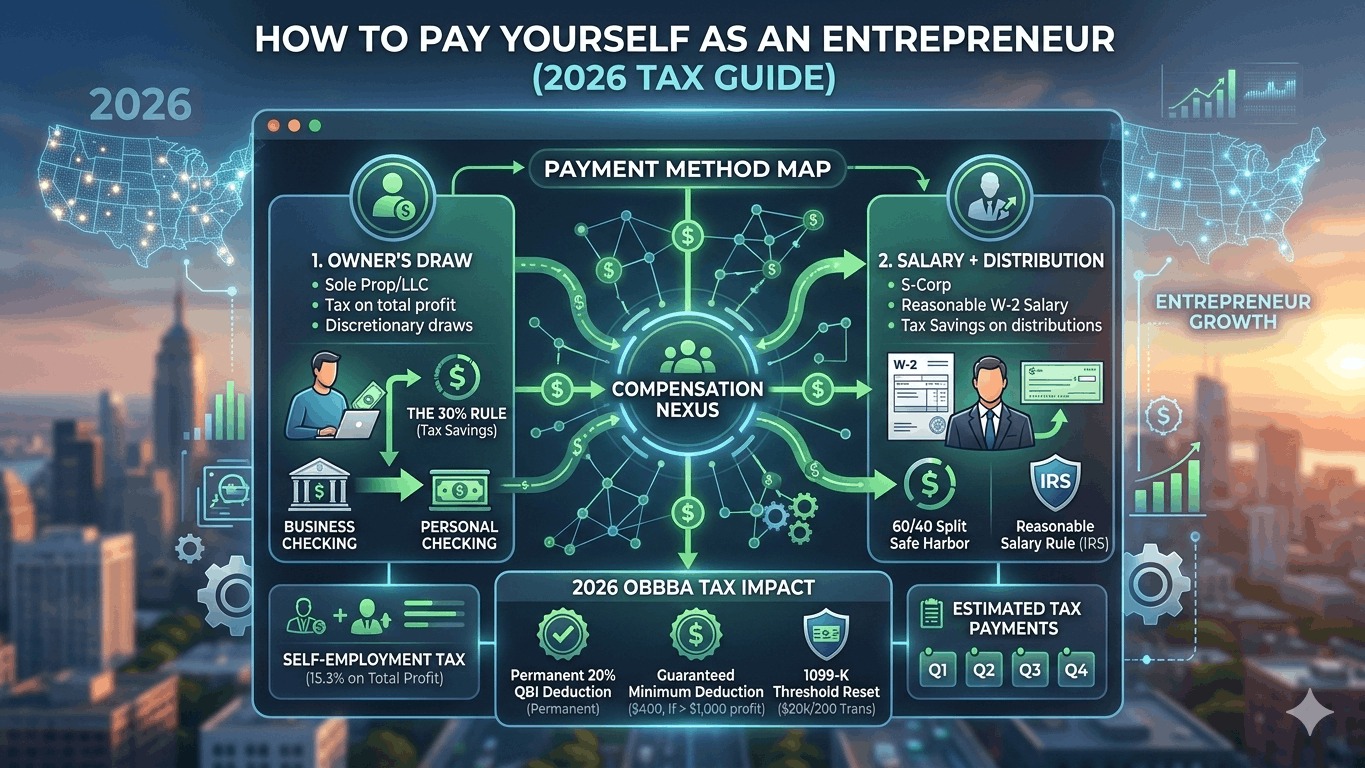

1. Choose Your Method: Draw vs. Salary

In 2026, your business structure dictates your payment "bucket." Mixing these up is one of the fastest ways to trigger an IRS audit.

| Structure | Payment Method | 2026 Tax Reality |

|---|---|---|

| Sole Proprietor / Single-Member LLC | Owner's Draw | You are taxed on total profit, not what you withdraw. |

| S-Corporation | Salary + Distribution | You must pay yourself a "Reasonable Salary" via W-2. |

| Partnership | Guaranteed Payments | Fixed payments for services, regardless of profit. |

| C-Corporation | Salary + Dividends | Subject to "Double Taxation" (Corporate + Personal). |

2. The 2026 OBBBA Tax Impact

The One Big Beautiful Bill Act has introduced three game-changers for how you calculate your pay this year:

- Permanent QBI Deduction: The 20% Qualified Business Income deduction is now permanent. This means for every $100 you "earn" in profit, you only pay income tax on $80.

- The $400 Guaranteed Deduction: Starting in 2026, the OBBBA guarantees a minimum $400 QBI deduction for any active business owner with at least $1,000 in profit—even if you'd otherwise be phased out.

- 1099-K Threshold Reset: If you pay yourself via apps like Venmo or PayPal, the reporting threshold has been restored to $20,000. You won't get a 1099-K for small, casual transfers, but you must still report them as income.

3. How to Execute an Owner’s Draw (Sole Prop/LLC)

If you aren't on a formal payroll, follow this "Clean Path" to move money:

- Calculate Net Profit: Total Revenue minus 2026 Expenses (including the now 100% bonus depreciation for equipment).

- The 30% Rule: Transfer 30% of that profit into a dedicated Tax Savings Account.

- The Transfer: Move the remaining funds from your Business Checking to Personal Checking.

- The Label: In your accounting software (QuickBooks/Xero), categorize the transaction as "Equity: Owner's Draw." It is not a business expense.

4. The "Reasonable Salary" Rule (S-Corps)

For S-Corp owners, the IRS is watching to ensure you don't take a tiny salary to avoid payroll taxes. In 2026, "Reasonable" is defined by:

- Market Rate: What would you pay a stranger to do your job?

- 2026 Inflation Adjustments: Ensure your salary keeps pace with the 2026 cost-of-living indices.

- The Split: A common "Safe Harbor" is the 60/40 Split (60% of profit as Salary, 40% as Distributions).

Quotes & Taglines

- "Profit is what the business makes; Pay is what you deserve."

- "Don't starve the business, but don't ignore the founder."

- "In 2026, your tax account should be your most consistent 'employee'."

- "A predictable pay schedule is the mark of a professional."