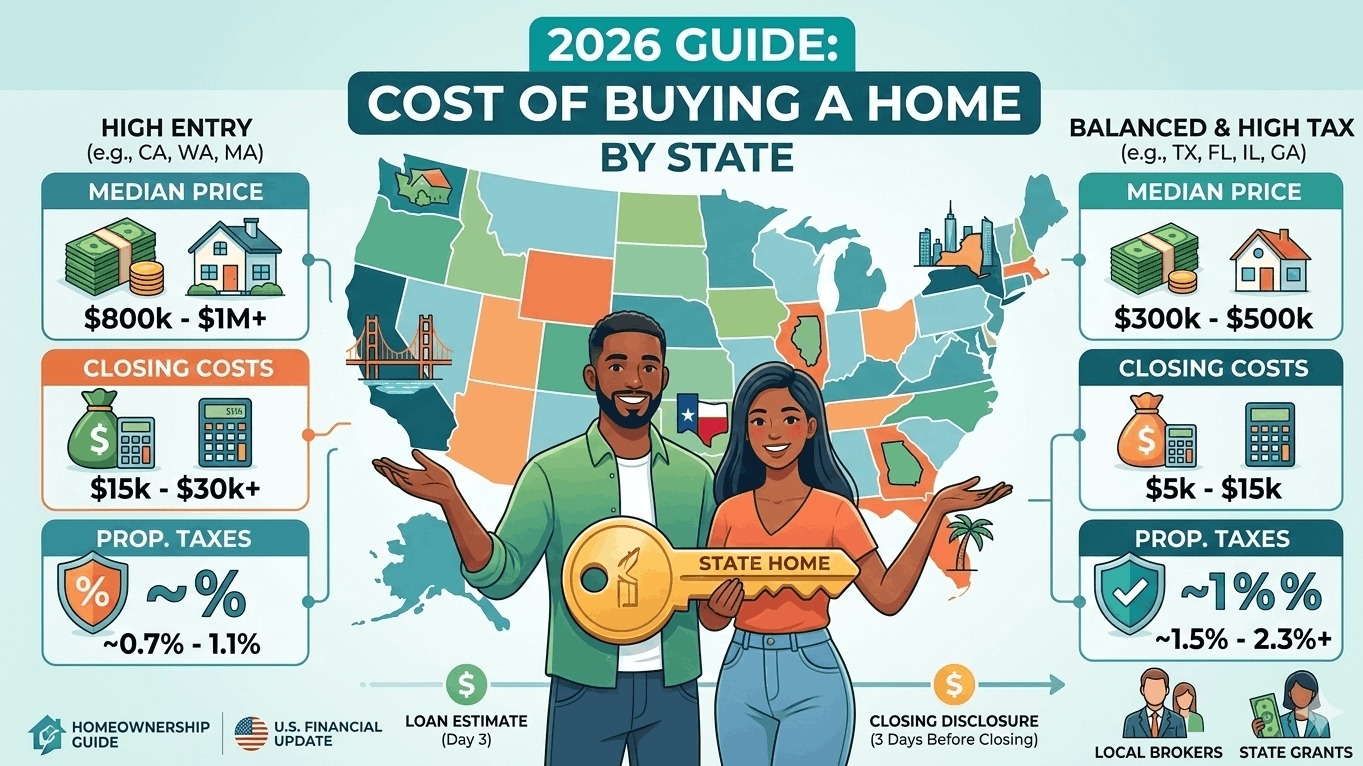

The cost of homeownership in the United States varies dramatically depending on where you plant your roots. In 2026, as the national housing market enters a period of stabilization with mortgage rates averaging 6.3%, the "all-in" price of a home—including the purchase price, closing costs, and recurring taxes—differs by hundreds of thousands of dollars across state lines.

This guide compares the 2026 costs for four of the most popular states: New York, California, Texas, and Florida.

1. California: High Entry, Lower Tax Percentage

California remains the most expensive market in the lower 48. While the median price nears $900,000, the state's property tax rate is surprisingly moderate due to legislative protections (like Prop 13).

- The Hidden Cost: Closing costs can be steep due to high home values, but the "cooling" market in 2026 has seen some price corrections in major metros like Los Angeles.

- Monthly Impact: High mortgage principal payments dominate the budget here.

2. New York: The Closing Cost Capital

Buying in New York involves complex legal and financial layers. New York ranks as one of the most expensive states for closing costs, often exceeding $13,000 for a typical home.

- The Tax Burden: NY homeowners face one of the nation's highest average property tax bills, with an annual average of $7,572.

- Regional Split: While NYC drives high prices, upstate regions offer affordability but often carry even higher effective property tax percentages.

3. Texas: No Income Tax, High Property Tax

Texas is a popular destination for those seeking more space for their dollar. However, because Texas has no state income tax, it relies heavily on property taxes to fund local services.

- The Reality Check: An effective property tax rate of 1.81% means a $400,000 home in Texas could cost you nearly $7,000 a year in taxes—double what you might pay for a similar home in Florida.

- Closing Costs: Generally lower and more competitive than the coasts.

4. Florida: The "Cooling" Sunbelt

After years of rapid appreciation, Florida’s market is showing signs of softening in 2026, with prices in major cities (except Miami) beginning to dip.

- The All-In Cost: Florida offers a balanced middle ground with a median budget around $480,000 and a moderate property tax rate of 0.89%.

- The Insurance Factor: While property taxes are manageable, homeowners in Florida must budget heavily for homeowners insurance, which remains significantly higher than the national average due to climate risks.

5. Washington: High Entry, No Income Tax

Washington continues to be a magnet for the tech sector, keeping median home values well above the national average. Like Texas, Washington has no state income tax, making it attractive for high-earners, though the entry cost for real estate is much higher.

- The Closing Cost Spike: Because closing costs are percentage-based (2%–5%), a median-priced home in the Seattle metro area can require nearly $30,000 at the closing table.

- Property Taxes: Relatively moderate, helping to offset the lack of income tax for those with high home equity.

6. Massachusetts: The Premium Education & Tech Hub

Massachusetts remains one of the most expensive states in the country, with an average sale price nearing $778,000 in early 2026.

- The "Slow" Market Advantage: Unlike the frenzy of previous years, the 2026 Massachusetts market has seen a slight increase in "days on market," giving buyers more room to negotiate inspections and repairs.

- Regional Variation: While Greater Boston prices are astronomical, western cities like Springfield offer a "starter" tier around $280,000, though these are becoming increasingly rare.

7. Illinois: Affordable Housing, Heavy Tax Burden

Illinois offers some of the most accessible median home prices in the Midwest, frequently hovering around the $290,000 mark. However, it carries one of the highest effective property tax rates in the nation.

- The "Second Mortgage" Effect: In counties like Cook or Lake, property taxes can effectively act as a "second mortgage" payment. A $300,000 home might carry an annual tax bill of $7,000+, significantly impacting monthly affordability.

- Inventory: Supply has remained tighter in Illinois than in other Midwest states, keeping prices from dipping despite high taxes.

8. Georgia: The Southeast’s Balanced Option

Georgia has seen a slight price correction in 2026, with average home values dipping about 1.9% year-over-year. This makes it a prime target for first-time buyers looking for value.

- The Sweet Spot: With a median price around $330,000 and a property tax rate under 1%, Georgia offers one of the best "all-in" affordability ratios in the country.

- Atlanta vs. Rural: Much of the state's cost is driven by the Atlanta metro area; however, mid-tier cities like Gainesville or Columbus offer entry points below $250,000.