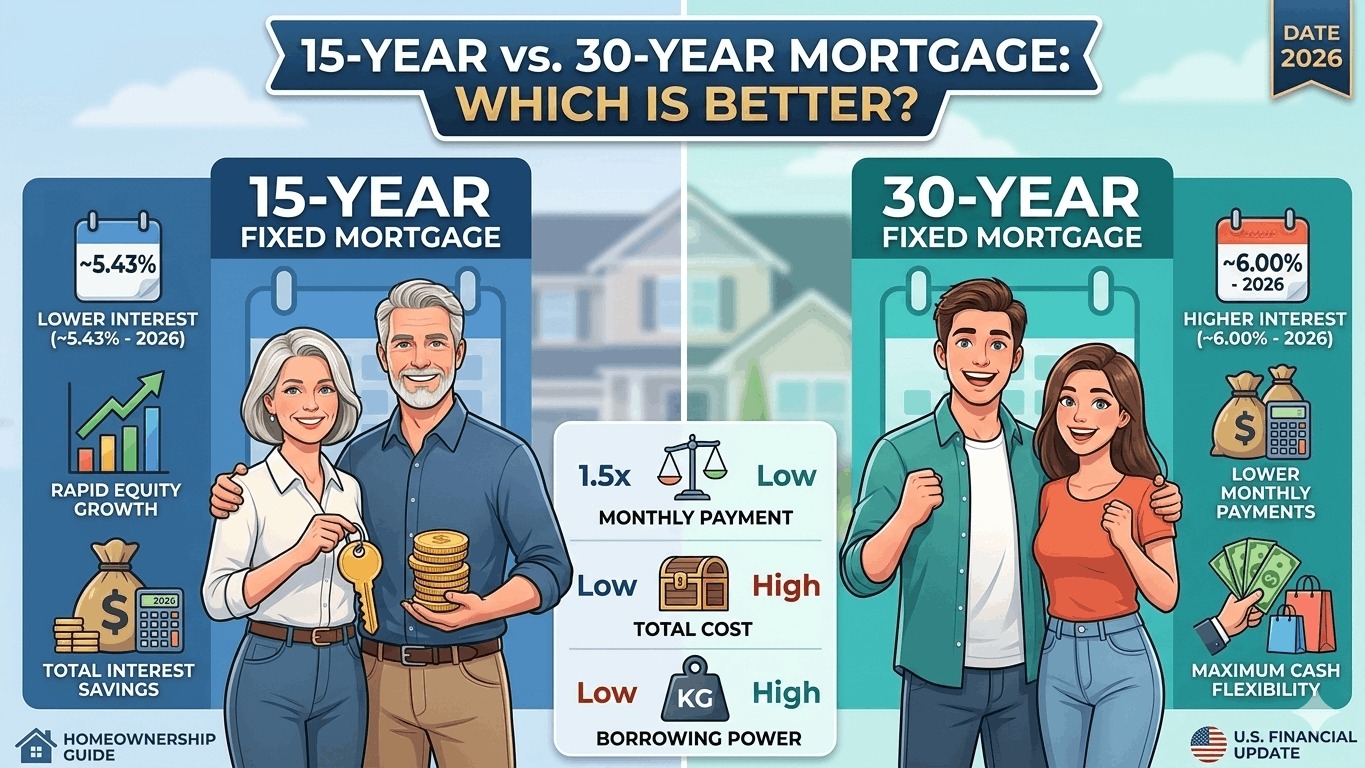

15-Year vs. 30-Year Mortgage: Which Is Better? (2026 Guide)

In the 2026 housing market, choosing between a 15-year and a 30-year mortgage is one of the most significant financial decisions you will make. With 30-year fixed rates currently hovering around 6.00% and 15-year rates significantly lower at roughly 5.43%, the "best" choice depends entirely on whether you prioritize monthly cash flow or long-term wealth building.

This comprehensive guide explores the math, the lifestyle implications, and the strategic "middle ground" for American homebuyers this year.

1. The Core Differences at a Glance

| Feature | 15-Year Fixed Mortgage | 30-Year Fixed Mortgage |

|---|---|---|

| Average Interest Rate (March 2026) | ~5.43% | ~6.00% |

| Monthly Payment | Significantly Higher (approx. 1.5x) | Lower and More Manageable |

| Total Interest Paid | Lowest | Highest |

| Equity Growth | Rapid | Slow (Initial years are interest-heavy) |

| Borrowing Power | Lower (due to higher DTI impact) | Higher (allows for a more expensive home) |

2. The Case for the 15-Year Mortgage

The 15-year mortgage is the "wealth-builder's" choice. Because you are compressed into a shorter repayment window, your money works harder for you from day one.

The "Interest Gap"

Lenders view 15-year loans as less risky because the debt is off their books in half the time. As of March 2026, you can typically secure a rate about 0.50% to 0.75% lower than a 30-year term.

Accelerated Equity

In a 30-year loan, the majority of your early payments go toward interest. In a 15-year loan, a much larger portion of your very first check goes toward the principal. This means if you need to sell or use a Home Equity Line of Credit (HELOC) in five years, you will have significantly more cash available.

Total Savings Example

Imagine a $400,000 loan:

- 30-Year @ 6.00%: You’ll pay roughly $463,000 in total interest over the life of the loan.

- 15-Year @ 5.43%: You’ll pay roughly $185,000 in total interest.

- The Result: Choosing the shorter term saves you over $278,000—the price of a second small home in some markets.

3. The Case for the 30-Year Mortgage

Despite the higher interest costs, the 30-year mortgage remains the most popular choice in the USA (accounting for nearly 90% of loans) for one reason: Flexibility.

Monthly Breathing Room

The 30-year term offers the lowest possible monthly payment. In a 2026 economy where inflation remains a concern, having an extra $800 to $1,200 in your pocket every month provides a safety net for emergencies, home repairs, or investing in the stock market.

Buying More House

Because mortgage lenders calculate your eligibility based on your Debt-to-Income (DTI) ratio, the lower payment of a 30-year loan allows you to qualify for a higher purchase price. If your dream home costs $500,000 but a 15-year payment on that amount exceeds 36% of your income, the 30-year loan may be your only path to that specific property.

4. The "Hybrid Strategy": The Best of Both Worlds

Many savvy 2026 buyers are opting for a 30-year mortgage but paying it like a 15-year.

Most U.S. mortgages do not have prepayment penalties. By taking the 30-year loan, you secure the flexibility of a lower required payment. However, if you have a high-income month or receive a bonus, you can apply extra principal payments.

- The Benefit: If you hit a financial rough patch (job loss or medical emergency), you can drop back to the lower 30-year payment without penalty.

- The Catch: You won't get the lower interest rate (5.43%) associated with the 15-year product, but you still save massively on interest by shortening the effective life of the loan.

5. Which One Is Right for You?

Choose a 15-Year Mortgage If:

- You are established in your career with a stable, high income.

- You are buying a "forever home" and want to be debt-free before retirement.

- You value "guaranteed" savings (interest avoidance) over the potential returns of the stock market.

Choose a 30-Year Mortgage If:

- You are a first-time buyer and need the lowest entry cost.

- You prefer to keep your cash "liquid" for other investments or business ventures.

- You are buying a "starter home" and plan to move or upgrade within 5 to 7 years.