Standard budgeting advice usually starts with: "Step 1: Write down your monthly take-home pay." But what if that number changes every 30 days? For freelancers, real estate agents, or small business owners, traditional budgeting feels like trying to hit a moving target.

The key to managing an irregular income isn't predicting exactly what you'll make—it's building a system that can handle both the "feast" and the "famine" months.

1. Calculate Your "Baseline" Expenses

When your income is unpredictable, you must know your absolute "floor." This is the minimum amount of money you need to keep the lights on and food on the table.

- Fixed Costs: Rent/mortgage, insurance, utilities, and minimum debt payments.

- Variable Essentials: A modest grocery budget and basic transportation.

- Non-Essentials: Subscriptions, dining out, and hobbies (these are the first to go during a lean month).

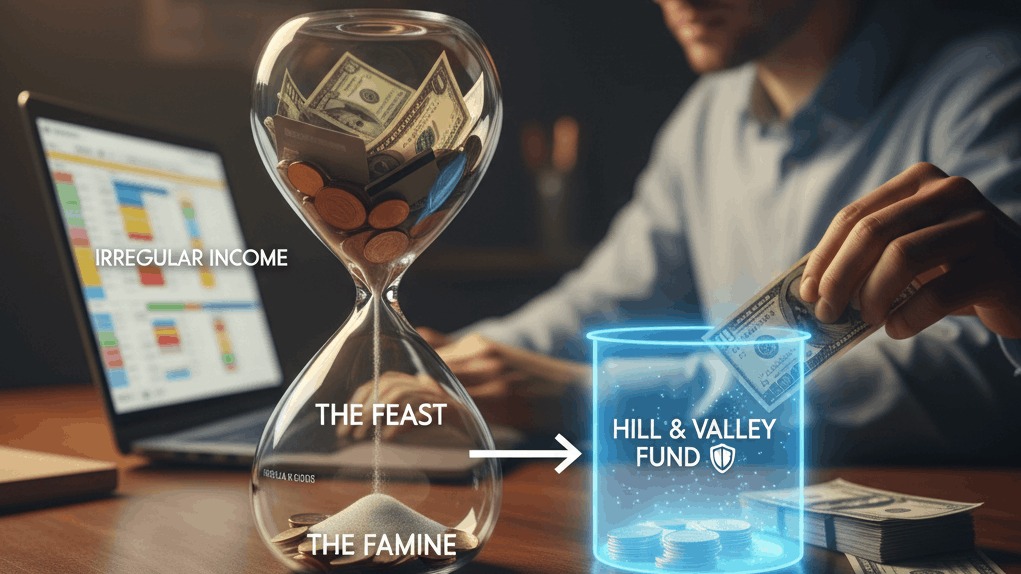

2. The "Hill and Valley" Fund

This is the secret weapon for variable earners. Also known as a Sinking Fund for Income, this is a separate account where you "park" extra money from high-earning months to cover the shortfall in low-earning months.

- During the Feast: If you earn $2,000 more than your average month, don't spend it. Move it to your Hill and Valley account.

- During the Famine: If you are $500 short of your baseline expenses, "pay yourself" from this fund.

3. Use a "Priority-Based" Budget (The Zero-Based Method)

Instead of allocating money you expect to get, only budget the money you already have in your bank account.

When a check clears, ask yourself: "What does this money need to do for me before I get paid again?"

- Give every dollar a job.

- Prioritize the most urgent "jobs" (like rent) first.

- If you have money left over after the essentials, move it to your "Hill and Valley" fund or your emergency savings.

4. Taxes Are Not Your Money

One of the biggest traps for irregular earners is spending the full amount of a client check.

- The 25-30% Rule: Set aside at least 25% of every single payment into a separate "Tax Savings" account immediately.

- Pay Quarterly: To avoid a massive bill (and potential penalties) in April, pay your estimated taxes to the IRS every quarter.

5. Pay Yourself a "Salary"

As your business or freelance work stabilizes, stop living directly off your business account.

- Deposit all income into a Business Savings Account.

- Set a fixed "salary" for yourself based on your average lowest month.

- Transfer that fixed amount to your Personal Checking Account on the 1st and 15th. This creates an artificial sense of stability that makes personal budgeting much easier.

Here are 10 powerful quotes for “How to Budget When Income Is Irregular”

- “When income is unpredictable, discipline becomes your stability.”

- “Budgeting on irregular income isn’t about perfection — it’s about preparation.”

- “Plan for the lowest month, celebrate the highest month.”

- “Consistency in planning creates calm in uncertainty.”

- “Irregular income requires regular strategy.”

- “In fluctuating seasons, your budget becomes your anchor.”

- “Save more in strong months to protect your weak ones.”

- “Control what you can — especially your spending.”

- “Flexibility is the secret weapon of every successful irregular earner.”

- “A variable income doesn’t mean variable discipline.”