When people first start investing, most attention goes toward stocks.

Stocks are exciting. They generate headlines, dramatic gains, and constant market discussion. Bonds, on the other hand, usually sound slower and less interesting.

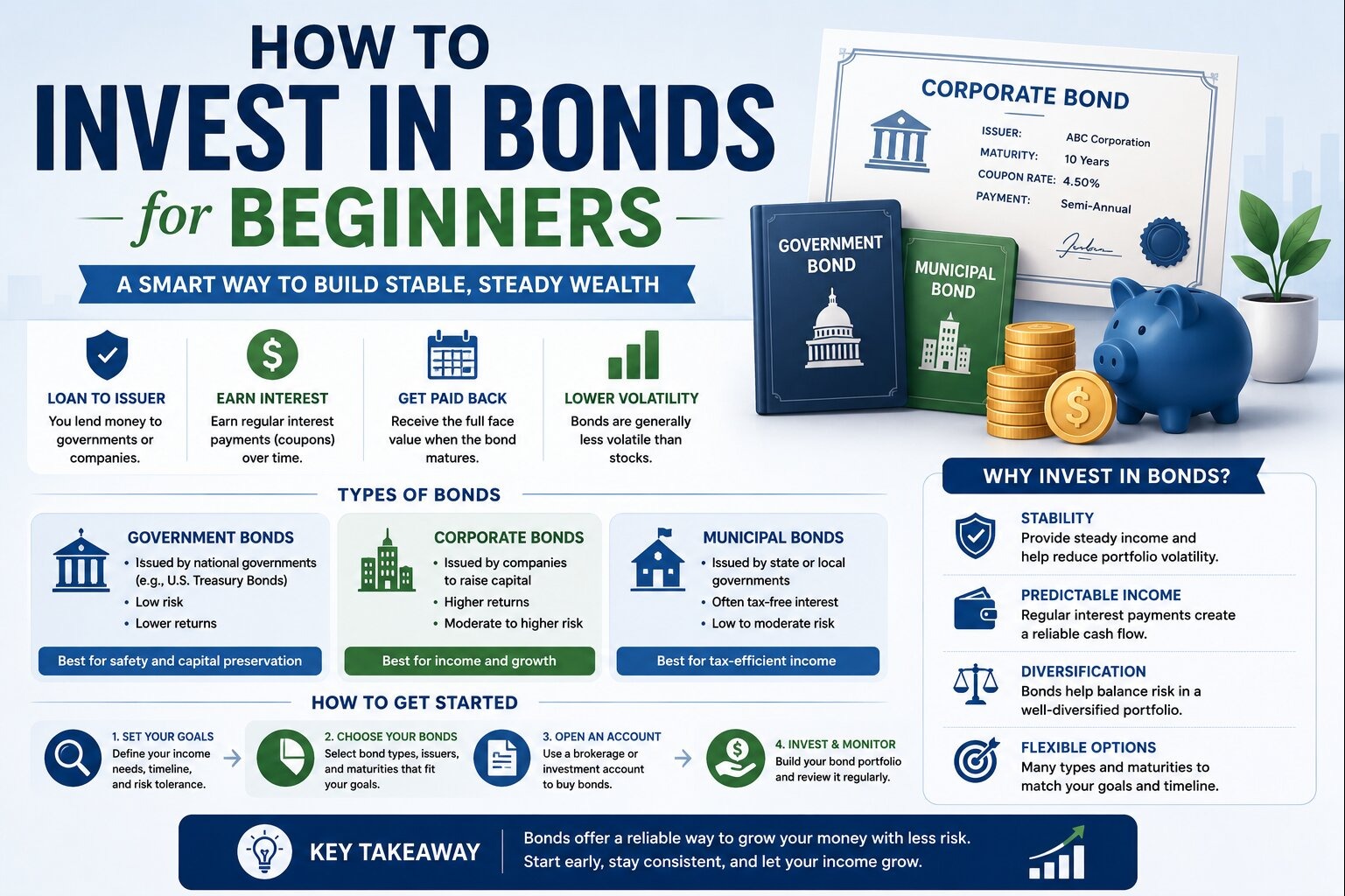

But bonds play a very important role in investing.

In fact, many experienced investors rely on bonds to provide:

- Stability

- Predictable income

- Lower portfolio volatility

- Diversification

And honestly, bonds become much more interesting once you understand how they actually work. They may not always deliver explosive returns like growth stocks, but they can help investors build more balanced and resilient portfolios over time.

What Is a Bond?

A bond is essentially a loan.

When you buy a bond, you are lending money to:

- A government

- A corporation

- A municipality

- Another organization

In return, the issuer agrees to:

- Pay interest regularly

- Repay the original amount later

The original investment amount is usually called the principal or face value.

How Bonds Work

Here’s a simple example:

- You buy a $1,000 bond

- Interest rate = 5%

- Bond maturity = 10 years

That means:

- You receive $50 annually in interest

- After 10 years, you get your original $1,000 back

The interest payment formula looks like this:

Annual\ Interest = Principal \times Interest\ Rate

In this example:

Annual\ Interest = 1000 \times 0.05 = 50

Compared to stocks, bonds are generally considered lower-risk investments, although they are not risk-free.

Why Investors Buy Bonds

Bonds serve several important purposes.

Income Generation

Many bonds provide predictable interest payments, making them attractive for:

- Retirees

- Conservative investors

- Income-focused portfolios

Portfolio Stability

Bonds often fluctuate less than stocks.

During major stock market declines, bonds sometimes help reduce overall portfolio losses.

Diversification

Stocks and bonds often behave differently under various economic conditions.

Combining both may improve overall portfolio balance.

You can learn more about balanced investing in Investment Portfolio Allocation by Age.

Main Types of Bonds

There are several different bond categories beginners should understand.

| Bond Type | Issuer | Typical Risk Level |

|---|---|---|

| Government Bonds | National governments | Lower |

| Municipal Bonds | Local governments | Lower to moderate |

| Corporate Bonds | Companies | Moderate to higher |

| High-Yield Bonds | Riskier companies | Higher |

Government Bonds

Government bonds are issued by national governments.

In many countries, these are considered among the safest investments because governments generally have strong ability to repay debt.

Examples include:

- U.S. Treasury bonds

- UK Gilts

- Government securities in other countries

Government bonds often provide:

- Lower risk

- Lower yields

- Greater stability

Corporate Bonds

Corporate bonds are issued by companies.

These bonds usually offer:

- Higher interest rates

- Greater income potential

- More risk compared to government bonds

The risk depends heavily on the company’s financial strength.

Strong financially stable companies typically pay lower yields because default risk is lower.

Riskier companies must offer higher yields to attract investors.

What Is Bond Yield?

Bond yield refers to the return investors receive from a bond.

Yield can become confusing because bond prices move after issuance.

Generally:

- Bond prices rise → yields fall

- Bond prices fall → yields rise

This inverse relationship is one of the most important concepts in bond investing.

Understanding Bond Maturity

Maturity refers to how long until the bond repays its principal.

| Bond Type | Typical Time Frame |

|---|---|

| Short-Term | Under 3 years |

| Medium-Term | 3–10 years |

| Long-Term | 10+ years |

Longer-term bonds usually offer:

- Higher yields

- Greater sensitivity to interest rates

Shorter-term bonds generally provide:

- Lower risk

- More stability

- Lower yields

Interest Rates and Bond Prices

Bond prices are heavily influenced by interest rates.

When Interest Rates Rise

Existing bonds with lower rates become less attractive.

As a result:

- Bond prices usually fall

When Interest Rates Fall

Older bonds with higher rates become more valuable.

As a result:

- Bond prices usually rise

This relationship surprises many beginners because they assume bonds always stay stable.

In reality, bond prices can fluctuate significantly depending on economic conditions.

Credit Ratings Matter

Bond issuers receive credit ratings that help investors evaluate risk.

Higher-rated bonds generally have:

- Lower default risk

- Lower yields

Lower-rated bonds offer:

- Higher yields

- Greater risk

Common rating agencies analyze:

- Financial health

- Debt levels

- Cash flow stability

Understanding company strength also connects with How to Evaluate Company Financial Statements.

What Is Bond Default Risk?

Default risk refers to the possibility that the issuer fails to:

- Pay interest

- Repay principal

Government bonds from stable countries usually carry lower default risk than corporate bonds.

High-yield bonds offer higher returns partly because default risk is higher.

Bond Funds vs Individual Bonds

Beginners often choose between:

- Individual bonds

- Bond funds or ETFs

Individual Bonds

Advantages:

- Predictable maturity

- Direct ownership

- Fixed repayment schedule

Disadvantages:

- Less diversification

- More research required

Bond Funds and ETFs

Advantages:

- Diversification

- Easier management

- Broad exposure

Disadvantages:

- No fixed maturity date

- Prices fluctuate continuously

For many beginners, bond ETFs provide a simpler starting point.

How Much of a Portfolio Should Be in Bonds?

This depends on:

- Age

- Risk tolerance

- Financial goals

- Time horizon

Generally:

- Younger investors often hold fewer bonds

- Older investors may increase bond exposure gradually

You can explore broader allocation ideas in Investment Portfolio Allocation by Age.

Bonds and Risk Reduction

Bonds are commonly used to reduce overall portfolio volatility.

For example:

- Stocks may fall sharply during recessions

- Bonds sometimes remain more stable

This does not mean bonds never lose value. But they often behave differently than stocks, which supports diversification.

This aligns closely with principles discussed in How to Reduce Investment Risk.

Real-World Example

Imagine two investors nearing retirement.

Investor A

- 100% invested in stocks

- Large market swings

- Higher growth potential

Investor B

- Mix of stocks and bonds

- Lower volatility

- More stable income

During a severe market downturn, Investor B may experience less emotional stress and smaller portfolio declines.

That stability matters greatly for many investors approaching retirement.

Common Bond Investing Mistakes

| Mistake | Potential Problem |

|---|---|

| Chasing high yields blindly | Greater default risk |

| Ignoring interest rate risk | Unexpected bond price declines |

| No diversification | Concentrated risk |

| Assuming bonds are risk-free | Misunderstanding market behavior |

| Overcomplicating bond investing | Poor decision-making |

Practical Tips for Beginners

Start Simple

Broad bond index funds or ETFs often work well for beginners.

Understand Your Goals

Different investors use bonds differently:

- Income

- Stability

- Diversification

- Capital preservation

Avoid Chasing Yield

Higher yields usually come with higher risk.

Think Long Term

Bond performance varies with interest rate cycles and economic conditions.

Bonds vs Stocks

| Feature | Bonds | Stocks |

|---|---|---|

| Ownership | Loan to issuer | Ownership stake |

| Income | Fixed interest | Variable dividends |

| Risk | Usually lower | Usually higher |

| Growth Potential | Lower | Higher |

| Volatility | Lower | Higher |

Both asset classes serve different purposes within a balanced portfolio.

Final Thoughts

Bonds may not receive as much excitement as stocks, but they remain an important part of investing for many people.

They can provide:

- Stable income

- Portfolio diversification

- Lower volatility

- Greater financial balance

For beginners, understanding bonds helps create more complete and resilient investment strategies rather than relying entirely on stock market growth.

And honestly, one of the biggest lessons investors eventually learn is that successful investing is not always about maximizing returns at all costs. Sometimes it’s about building a portfolio stable enough to stay invested confidently through all types of market conditions.