In the 2026 financial climate, with average credit card APRs often exceeding 22%, many Americans feel like they are running on a treadmill—making payments every month but watching their balances stay the same. This is where a balance transfer acts as a "pause button" on interest, allowing you to actually touch the principal of your debt.

A balance transfer isn't "free money," but when used with a specific plan, it is one of the most powerful tools in the debt-reduction toolkit.

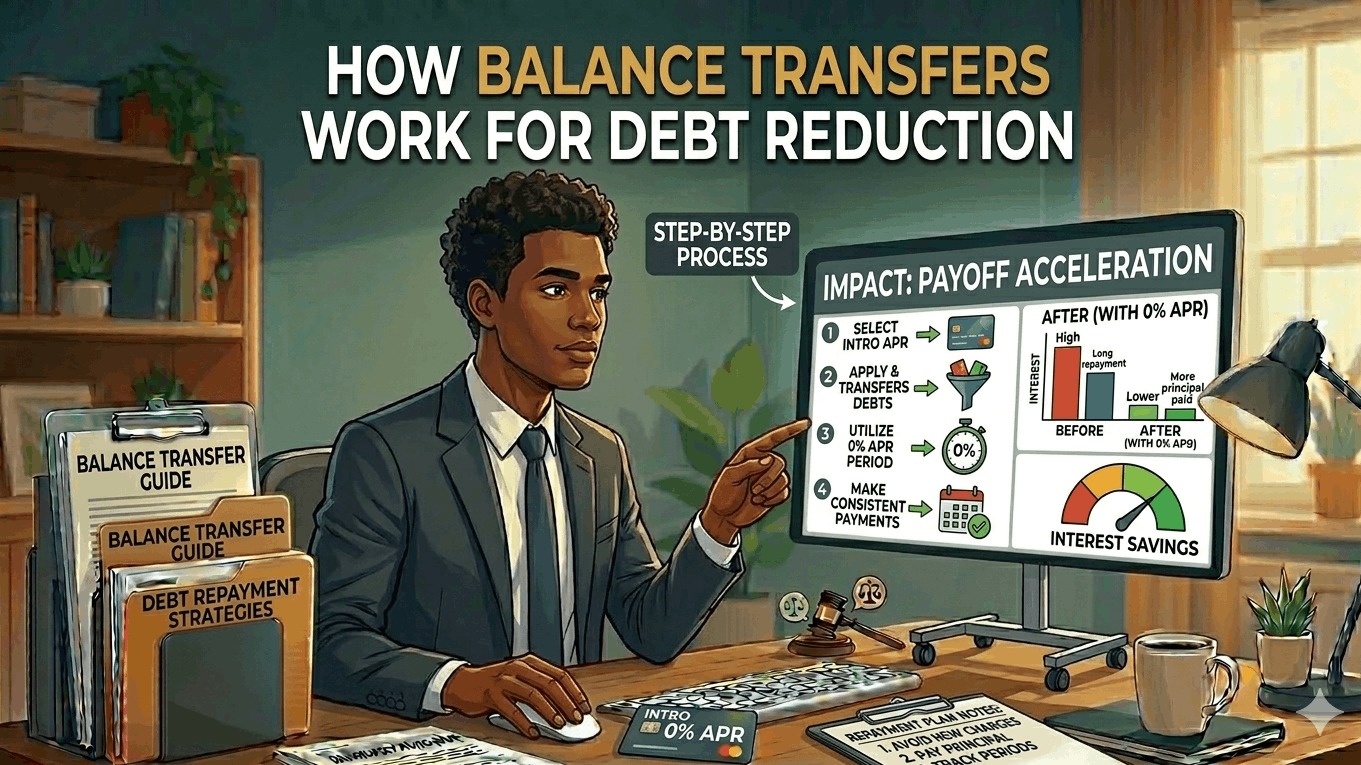

1. The Core Concept: Shifting, Not Erasing

A balance transfer is the process of moving high-interest debt from one (or multiple) credit cards to a new card with a much lower interest rate—ideally 0% APR.

- The Swap: You aren't paying off the debt; you are moving it. For example, moving a $5,000 balance from a card at 24% APR to a 0% APR card stops the roughly $100 per month in interest charges from accruing.

- The Principal Focus: Without interest eating your payment, 100% of every dollar you send to the bank goes toward the original balance.

2. The Cost of Doing Business: Transfer Fees

In 2026, most major banks (Chase, Citi, Wells Fargo) charge a Balance Transfer Fee.

- Standard Rates: Expect to pay between 3% and 5% of the total amount you transfer.

- The Math: If you transfer $5,000 with a 4% fee, $200 is added to your new balance immediately.

- Is it worth it? Usually, yes. Paying $200 once is significantly cheaper than paying $100 in interest every month for a year or more.

3. The 2026 "Intro Window"

Introductory periods in 2026 are competitive, often ranging from 12 to 21 months.

- Top 2026 Offers: Cards like the Wells Fargo Reflect® and Citi Simplicity® have maintained their status as "marathon" cards, offering up to 21 months of 0% interest.

- The Cliff: Once the intro period ends, the remaining balance will jump to the standard APR (often 18%–28%). Your goal must be to hit $0 before that clock runs out.

4. How a Balance Transfer Affects Your Credit Score

Many borrowers worry that opening a new card will hurt their credit. In reality, it’s a “short-term dip for a long-term gain.”

- The Dip: Applying for a new card triggers a Hard Inquiry, which might drop your score by 5–10 points temporarily.

- The Gain: By opening a new card, you increase your Total Available Credit. This lowers your Credit Utilization Ratio—the second most important factor in your FICO score. As you pay down the transferred balance, your score will typically climb much higher than it was before.

5. The Step-by-Step Execution Plan

- Audit Your Debt: List your current cards, their balances, and their APRs.

- Check Your Score: You generally need a score of 670 or higher (Good to Excellent) to qualify for the best 0% offers.

- Apply for a "Different" Bank: You usually cannot transfer a balance between two cards from the same issuer (e.g., you can't move a Chase Slate balance to a Chase Freedom).

- Initiate the Transfer: Once approved, you provide the account numbers of your old cards to the new bank. The process takes 7–14 days.

- The "One-Card Rule": Once the old card is at $0, do not close it. Closing old accounts can hurt your "Length of Credit History." Put the card in a drawer and don't use it.